Fiscal Year 2025

811

Loans Approved

$739M

Total Value

An SBA 7(a) loan for dentists can help qualified practice owners access flexible financing for major growth, acquisition, and operating needs. The SBA 7(a) program is the U.S. Small Business Administration’s primary business loan program, and funds can be used for a wide range of eligible purposes, including real estate, equipment, working capital, business acquisition, debt refinancing, and ownership changes.

The loan itself is issued by an SBA-approved lender, not directly by the SBA. The SBA provides a guaranty to the lender, which can reduce lender risk and make financing more accessible for qualified borrowers. For most 7(a) loans, the SBA guaranty is up to 85% for loans of $150,000 or less and up to 75% for loans above $150,000.

7aSavvy helps dental borrowers get connected with SBA 7(a) lenders that fit the deal. Our lender-matching process is designed to make the search easier, especially for dentists who are trying to compare lender appetite, loan structure, and next steps without going bank to bank on their own.

Why Dentists Consider SBA 7(a) Financing

That is one reason many dentists look at SBA loans for dental practice financing. The program can be a fit when the borrower needs capital for more than one purpose, such as buying a dental office, acquiring an existing practice, upgrading equipment, refinancing eligible business debt, or covering working capital during a transition.

A conventional bank loan may be the right choice for some established practices. But when the transaction includes acquisition financing, real estate, equipment, and operating capital together, an SBA 7(a) dental practice loan may offer a more practical path for qualified borrowers.

Uses of SBA 7(a) Loans for Dentists

An SBA 7(a) loan for dentists can be used for many of the major expenses involved in starting, buying, expanding, or improving a dental practice. Because the program allows funds to be used for real estate, working capital, equipment, debt refinance, furniture, fixtures, supplies, and ownership changes, it can be a flexible option for dental practice financing.

Dental Practice Acquisition

Buying an existing dental practice is one of the most common reasons dentists consider SBA 7(a) financing. A practice acquisition may involve more than the purchase price alone. The deal can include dental equipment, patient records, goodwill, transition costs, leasehold improvements, and working capital for the first months after closing.

Office Buildout and Practice Improvements

Dental offices often require specialized layouts, plumbing, electrical work, treatment rooms, sterilization areas, imaging spaces, waiting rooms, and front-office improvements. Whether the goal is to open a new practice location or modernize an existing office, an SBA 7(a) loan may be used for improving real estate and buildings when the project meets program requirements.

Dental Equipment and Technology

Dental practices depend on high-cost equipment and technology. SBA 7(a) financing may be used for purchasing and installing machinery and equipment, as well as furniture, fixtures, and supplies.

Working Capital for Dental Practices

Even a strong dental practice can need working capital. Payroll, supplies, rent, insurance, marketing, software, lab fees, hiring, and transition expenses can all affect cash flow, especially during a startup, acquisition, relocation, or expansion. SBA 7(a) loans may be used for both short- and long-term working capital.

Business Debt Refinance

Some dental practices carry debt from equipment purchases, earlier expansion projects, or other business financing. An SBA 7(a) loan may be used to refinance current business debt when the refinance meets SBA and lender requirements.

Change of Ownership

A dental practice transition is not always a simple sale from one owner to another. It may involve buying out a partner, purchasing the remaining share of a practice, or completing a staged ownership transfer. SBA 7(a) financing may be used for complete or partial changes of ownership.

Real Estate Purchase or Refinance

Some dentists use SBA 7(a) financing to buy or refinance owner-occupied business real estate. For a dental practice, owning the building can provide more control over location, occupancy costs, future improvements, and long-term planning. An SBA 7(a) loan may be used for acquiring, refinancing, or improving real estate and buildings.

Multiple-Purpose Dental Practice Loans

Many dental financing needs do not fit neatly into one category. A dentist buying a practice may also need to upgrade equipment, renovate treatment rooms, purchase supplies, and keep working capital available after closing. The SBA 7(a) program allows multiple-purpose loans, which can make it practical for dentists who need one financing structure for several eligible uses.

SBA 7(a) Loans for Dentists Terms and Eligibility

How Much Can Dentists Borrow With an SBA 7(a) Loan?

The standard maximum loan amount for most SBA 7(a) loans is $5 million. That does not mean every dentist, dental group, or practice acquisition will qualify for the full amount. The final loan size depends on the borrower, the practice, the use of funds, repayment ability, lender underwriting, and SBA eligibility requirements.

For dental practice owners, that loan ceiling can create room for larger financing needs, such as buying an existing dental practice, purchasing owner-occupied real estate, completing a specialized office buildout, upgrading equipment, refinancing eligible business debt, or combining several approved uses into one loan request.

A dentist buying a practice may need capital for the purchase price, equipment, working capital, improvements, and transition costs. A growing practice may need funds for additional operatories, imaging technology, leasehold improvements, or a larger location. Because SBA 7(a) loans can support multiple eligible business purposes, they can be useful for dentists whose financing needs go beyond a simple equipment purchase.

SBA 7(a) Loan Repayment Terms for Dentists

Repayment terms under the SBA 7(a) program depend on how the loan proceeds are used. For loans involving real estate, terms may extend up to 25 years. Longer repayment structures can help reduce monthly debt service compared with shorter-term financing, which may matter for dentists managing payroll, lab costs, supplies, rent, insurance, and equipment expenses.

For non-real estate dental financing needs, 10 years is the maximum loan term. For multiple uses of proceeds including both real estate and non-real estate uses, the term will depend on the proportions of the different uses.

For dentists, the repayment structure is an important part of the decision. A loan that works on paper still needs to fit the practice’s actual cash flow. Lenders will usually consider whether the practice can support the debt while continuing to operate, invest in patient care, and manage day-to-day expenses.

SBA 7(a) Loan Qualifications for Dentists

The SBA 7(a) program is designed for eligible small businesses. In general, a business must operate for profit, be located in the United States, meet SBA size standards, show a need for the requested credit, and use the loan proceeds for a sound business purpose.

For dentists, basic eligibility is only the starting point. Lenders also review creditworthiness, repayment ability, the requested use of funds, and the strength of the business or transaction.

A dental SBA loan request may involve review of:

- The dentist’s ownership and operating experience

- Personal credit and financial profile

- Practice revenue and cash flow

- Tax returns and financial statements

- Production trends and patient base

- Purchase agreement or expansion plan

- Equipment and buildout costs

- Real estate details, if property is involved

- Working capital needs

- Debt service coverage and repayment ability

For a dental practice acquisition, lenders may also review seller financials, goodwill, transition plans, valuation basis, and whether the buyer can successfully take over the practice. For an expansion or office buildout, lenders may look at contractor estimates, project scope, location strength, and projected cash flow after the improvements are complete.

Important note:

Meeting SBA eligibility requirements does not guarantee approval. A dentist may meet the basic program rules and still need to satisfy lender underwriting standards.

SBA 7(a) Loans for Dentists: Pros and Cons

An SBA 7(a) loan for dentists can do more than help cover one expense. It can provide qualified dental practice owners with a flexible financing structure for larger projects that often require multiple types of capital.

For a dentist, one financing need may include a practice acquisition, equipment upgrades, office improvements, working capital, and transition costs. The SBA 7(a) program can support a wide range of eligible uses, including business purchase, real estate, equipment, working capital, eligible debt refinance, and ownership changes. That flexibility can make it a practical option for dentists who need funding that fits the full scope of a practice project.

That can be especially useful in dental practice financing, where the cost of growth is rarely limited to one line item. Buying a practice may also require new technology, updated operatories, a working capital cushion, and funds for a smooth patient and staff transition. Expanding an existing office may involve construction, equipment, furniture, software, and operating expenses before the new space is fully productive.

Repayment structure is another reason dentists consider SBA 7(a) financing. For loans involving real estate, terms may extend up to 25 years, which can help spread payments over a longer period than many shorter-term financing options. SBA 7(a) loans also include an SBA guaranty to the lender, which may help qualified borrowers access more advantageous financing when a conventional loan is not the right fit. For most 7(a) loans, the guaranty can be up to 85% for loans of $150,000 or less and up to 75% for loans above $150,000.

The tradeoff is that SBA 7(a) loans are not instant approvals. Borrowers should expect documentation, lender review, SBA eligibility checks, and underwriting. The program also has a standard maximum loan amount of $5 million, and the best conventional financing options may still be more attractive for some highly qualified borrowers with simple loan requests.

SBA 7(a) Loans vs. Other Dental Practice Financing Options

SBA 7(a) Loans vs. Conventional Dental Practice Loans

Both SBA 7(a) loans and conventional business loans can be used for dental practice financing, but they are not built the same way.

A conventional dental practice loan may be a good fit for borrowers with strong credit, stable cash flow, a clear operating history, and a loan request that fits neatly within a lender’s standard requirements. Some dentists may prefer conventional financing when they qualify for attractive terms without SBA support or when they want to avoid SBA program rules.

An SBA 7(a) loan may be more useful when the borrower needs a flexible structure or when the financing request includes several business purposes. For example, a dentist buying a practice may need funds for the acquisition itself, equipment updates, leasehold improvements, transition costs, and working capital. A dentist expanding an existing office may need capital for construction, new operatories, dental technology, and operating expenses during the project.

The SBA guaranty is one of the main differences. For most 7(a) loans, the SBA can guarantee up to 85% of loans of $150,000 or less and up to 75% of loans above $150,000. That guaranty helps reduce lender risk and may make financing more accessible for qualified borrowers who would not receive the same structure from a conventional loan.

The 7(a) program also includes a standard maximum loan amount of $5 million. That can provide room for many dental practice acquisitions, expansions, real estate purchases, and multi-purpose projects, although the final approved amount depends on the borrower, practice financials, use of funds, repayment ability, and lender underwriting.

For dentists, the comparison often comes down to fit. If the practice has a straightforward financing need and qualifies easily through a bank, a conventional loan may be worth comparing. If the request involves a practice purchase, ownership transition, real estate, equipment, working capital, or eligible refinance needs in one structure, or if qualification isn’t as easy, an SBA loan for dentists may be the stronger option to explore.

7aSavvy can help dental borrowers start that process through our SBA 7(a) lender-matching, making it easier to connect with lenders experienced with dental practice loans.

SBA 7(a) Loans vs. SBA 504 Loans for Dentists

SBA 7(a) loans and SBA 504 loans are both SBA-backed financing options, but they are designed for different purposes. That distinction matters for dentists comparing ways to fund a practice purchase, office property, expansion, or equipment project.

The SBA 7(a) program is generally the more flexible option. Funds may be used for eligible purposes such as business acquisition, real estate, working capital, equipment, furniture, fixtures, supplies, eligible business debt refinance, ownership changes, and multiple-purpose loans.

SBA 504 loans are more focused on major fixed assets. They are commonly used for projects such as buying land or buildings, constructing or improving facilities, and purchasing long-term machinery or equipment. However, SBA 504 loan proceeds cannot be used for working capital or inventory.

There are also loan structure differences. SBA 504 loans are partly delivered through Certified Development Companies, while SBA 7(a) loans are issued by typical lenders, like banks and credit unions. The standard maximum loan amount for SBA 7(a) financing is $5 million, while the maximum 504 loan amount is $11.25 million. SBA 504 loans are generally designed as long-term, partly fixed-rate financing for major fixed assets, while SBA 7(a) loans may have fixed or variable rates depending on the lender and loan structure.

For a dentist, the better option depends on the project. A dental office real estate purchase with limited additional needs may point toward 504 financing. A dental practice acquisition that also requires equipment, improvements, working capital, and transition funds may be better suited to the 7(a) program.

Because the right path is not always obvious at the start, 7aSavvy helps dentists get connected with SBA 7(a) lenders that are aligned with the size and purpose of the request. Our platform is designed for borrowers who want a more efficient way to explore SBA 7(a) financing.

SBA 7(a) Loan Program History

The SBA 7(a) loan program has been part of the small business financing landscape for decades. Its roots go back to the Small Business Act of 1953, which created the U.S. Small Business Administration and established federal support for small business lending. The program takes its name from Section 7(a) of that law, and it has developed into the SBA’s primary business loan program for helping small businesses access financing through approved lenders.

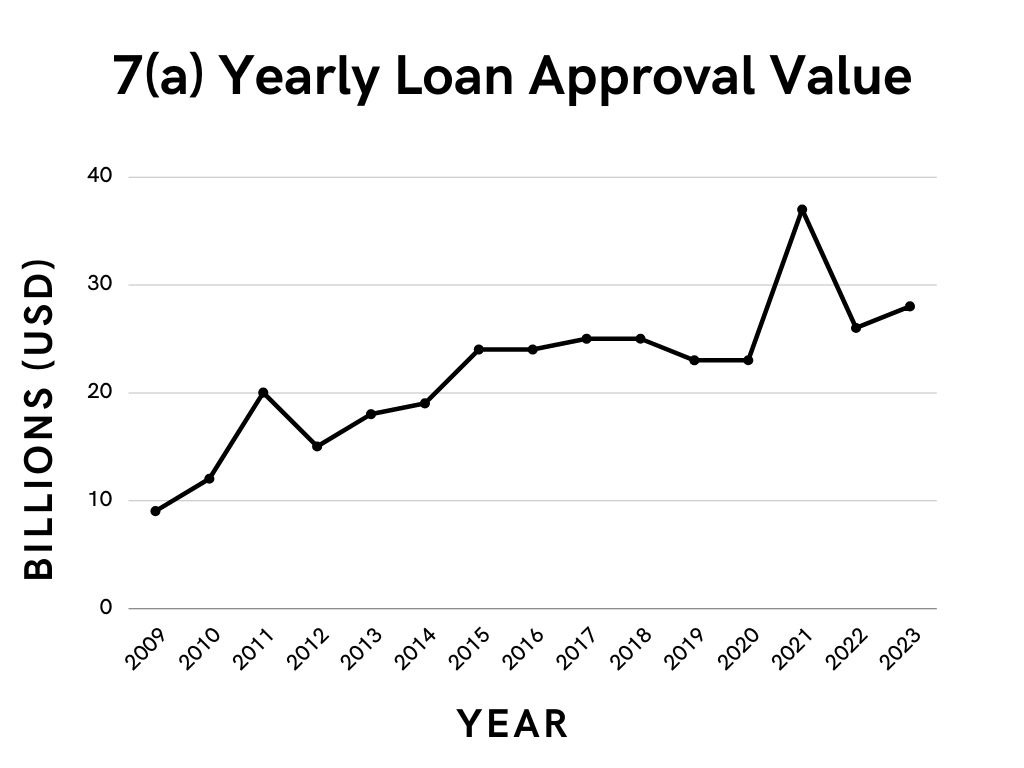

SBA 7(a) Loan Program Statistics

These are the year-by-year* statistics of the SBA 7(a) loan program from Fiscal Year 1992 to today, including the number of 7(a) loans approved and total approval amount.

| Fiscal Year | Loans Approved | Approval Amount |

| 1992 | 23,655 | $5,880,429,292 |

| 1993 | 26,291 | $6,690,995,672 |

| 1994 | 36,049 | $8,142,444,017 |

| 1995 | 55,548 | $8,251,957,812 |

| 1996 | 45,853 | $7,694,062,736 |

| 1997 | 45,288 | $9,461,352,612 |

| 1998 | 42,271 | $9,016,559,155 |

| 1999 | 43,634 | $10,146,109,913 |

| 2000 | 43,748 | $10,523,436,538 |

| 2001 | 42,958 | $9,894,022,393 |

| 2002 | 51,666 | $12,208,026,875 |

| 2003 | 67,306 | $11,268,200,031 |

| 2004 | 81,133 | $13,571,560,391 |

| 2005 | 95,900 | $15,223,525,886 |

| 2006 | 97,291 | $14,525,100,339 |

| 2007 | 99,606 | $14,292,141,213 |

| 2008 | 69,437 | $12,671,235,790 |

| 2009 | 41,288 | $9,191,044,339 |

| 2010 | 47,000 | $12,406,048,700 |

| 2011 | 53,710 | $19,640,298,400 |

| 2012 | 44,376 | $15,153,504,000 |

| 2013 | 46,395 | $17,865,672,500 |

| 2014 | 52,044 | $19,190,547,800 |

| 2015 | 63,461 | $23,583,863,400 |

| 2016 | 64,074 | $24,128,426,343 |

| 2017 | 62,430 | $25,447,458,500 |

| 2018 | 60,354 | $25,372,539,100 |

| 2019 | 51,907 | $23,175,811,000 |

| 2020 | 42,298 | $22,549,825,700 |

| 2021 | 51,856 | $36,536,756,800 |

| 2022 | 47,678 | $25,693,805,700 |

| 2023 | 57,362 | $27,515,666,000 |

| 2024 | 70,242 | $31,124,036,200 |

| 2025 | 78,078 | $37,287,816,200 |

Source: SBA, 7(a) & 504 FOIA

*U.S. Federal Government fiscal years

SBA 7(a) Loans On the Rise

The SBA 7(a) loan program has seen outstanding recent growth, with the annual total value of approved loans tripling in the last 15 years. Not bad for a program that’s been around since 1953!