Fiscal Year 2025

84

Loans Approved

$73M

Total Value

Starting, buying, or expanding a private school requires more than a strong educational mission. It takes reliable funding for real estate, classrooms, staffing, equipment, technology, curriculum resources, and the everyday operating costs that keep the school running smoothly.

An SBA 7(a) loan for private schools can be a practical financing option for eligible education businesses that need flexible capital. The SBA 7(a) program is the U.S. Small Business Administration’s main loan program for small businesses, with loans made through approved lenders rather than directly by the SBA. For most 7(a) loans, the SBA will guarantee 85% of loans of $150,000 or less and 75% of loans above $150,000, which helps reduce the lender’s risk for qualified borrowers.

For private school owners, childcare education operators, preschool groups, specialty learning centers, and investors acquiring an established school, lender support can matter. Education businesses often have unique financing needs, from purchasing a school building to renovating classrooms, upgrading safety systems, adding playgrounds or labs, buying furniture and fixtures, or covering short- and long-term working capital.

Why Private School Owners Look at SBA 7(a) Financing

Financing a private school is different from funding many other small businesses. Lenders may need to understand enrollment trends, tuition revenue, licensing or accreditation requirements, facility needs, staffing costs, and whether the school is being launched, acquired, expanded, or refinanced. A conventional business loan may fit some education businesses, but an SBA 7(a) loan for private schools can be worth considering when the financing need is more complex than a simple property purchase.

Private schools often need capital that can support both long-term growth and day-to-day operations. A school may need funding to buy a building, renovate classrooms, improve outdoor learning areas, purchase furniture and equipment, invest in technology, refinance eligible business debt, or manage working capital during enrollment cycles. Because the SBA 7(a) program allows funds to be used for several business purposes, it can be a flexible option for qualified school owners and operators.

Uses of SBA 7(a) Loans for Private Schools

An SBA 7(a) loan for a private school may be used for needs such as:

Private School Acquisition

Buying an existing private school can be one of the main reasons borrowers explore SBA 7(a) financing. This may include purchasing a preschool, K-12 private school, tutoring center, specialty education business, or another eligible for-profit school operation, depending on SBA requirements and lender review.

Facility Purchase or Expansion

Private schools often need dedicated space that supports classrooms, offices, activity areas, outdoor learning, and student services. SBA 7(a) financing may be used to acquire, refinance, or improve real estate and buildings, which can make it useful for school owners purchasing a campus, expanding into a larger property, or improving an existing facility.

Renovations and School Improvements

A growing school may need capital for classroom buildouts, accessibility upgrades, security improvements, playground enhancements, science labs, libraries, cafeterias, administrative areas, or general building improvements. Because 7(a) proceeds can support improvements to real estate and buildings, the program may fit projects that help a private school create a safer, more functional learning environment.

Furniture, Fixtures, Equipment, and Supplies

Private schools regularly invest in desks, tables, classroom furniture, computers, learning technology, security systems, kitchen equipment, playground equipment, administrative tools, and other operating assets. SBA 7(a) funds may be used for machinery, equipment, furniture, fixtures, supplies, and related business needs, giving qualified school owners a way to finance more than just the building itself.

Working Capital

Enrollment cycles, staffing, curriculum purchases, marketing, insurance, utilities, and start-up periods can put pressure on cash flow. SBA 7(a) loans may be used for working capital, which can help eligible private schools manage short-term needs while supporting longer-term growth.

Debt Refinance

Some school owners use SBA financing to refinance eligible business debt into a structure that better fits the school’s cash flow. This can be especially helpful when prior financing was used for school improvements, expansion, equipment, or other business purposes and the borrower wants to explore a more suitable repayment structure.

Change of Ownership

If a transaction involves buying out a partner, purchasing a school from an existing owner, or completing a full or partial ownership transition, SBA 7(a) financing may be an option. For education entrepreneurs, this can make it easier to take over an established private school while also financing related business needs through the same loan request.

SBA 7(a) Loans for Private Schools Terms and Eligibility

How Much Can You Borrow?

The standard maximum loan amount for most SBA 7(a) loans is $5 million. Not every private school project will qualify for the maximum amount, and approval depends on the borrower, business financials, loan purpose, lender requirements, and SBA eligibility. Still, the program can give qualified private school owners meaningful room to finance acquisitions, real estate, renovations, equipment, refinancing, working capital, or a combination of eligible uses.

Repayment Terms and Prepayment Rules

Repayment terms for an SBA 7(a) loan for private schools depend on how the funds are used. If the loan includes real estate, the term may extend up to 25 years, which can help school owners spread out payments over a longer period than many conventional financing options.

That can be especially useful for private school borrowers purchasing a campus, expanding into a larger facility, or financing major building improvements. Education businesses often need time for enrollment growth, tuition revenue, staffing plans, and facility investments to translate into stronger cash flow. A longer repayment structure may make the financing easier to manage while the school continues to grow.

Private school owners should also understand how SBA 7(a) prepayment rules work. For loans with a maturity of 15 years or longer, a prepayment penalty will apply if the borrower voluntarily prepays 25% or more of the outstanding balance during the first three years after the first disbursement. The penalty is 5% in the first year, 3% in the second year, and 1% in the third year.

SBA 7(a) Loan Qualifications for Private Schools

The SBA 7(a) program is intended for eligible small businesses that meet SBA and lender requirements. In general, a private school borrower must:

- be an operating business

- operate for profit

- be located in the United States

- meet SBA size standards

- show a need for the requested credit

- use the loan proceeds for a sound business purpose

- be creditworthy and demonstrate a reasonable ability to repay the loan

For private schools, the lender review goes beyond basic eligibility. Lenders may also look at enrollment history, tuition revenue, student retention, operating expenses, facility condition, licensing or accreditation considerations, management experience, staffing needs, and whether the projected cash flow supports the requested debt.

Important note:

Meeting the general SBA requirements does not guarantee approval. Final eligibility for an SBA 7(a) loan for private schools depends on the business type, use of proceeds, borrower credit profile, repayment ability, available collateral, lender criteria, and SBA program rules.

SBA 7(a) Loans for Private Schools: Pros and Cons

An SBA 7(a) loan for private schools can give education business owners access to financing that supports both facilities and operations. Instead of being limited to one narrow use, the program can help eligible borrowers fund private school acquisitions, real estate purchases, renovations, equipment, furniture, fixtures, working capital, eligible debt refinancing, and changes of ownership.

That flexibility matters because private school financing is rarely one-dimensional. A school owner may need to purchase a building, improve classrooms, upgrade technology, buy desks and learning materials, support payroll, and manage enrollment-related cash flow at the same time. SBA 7(a) financing for private schools can make it possible to address those needs through one loan structure.

The program may also offer longer repayment terms, including up to 25 years when real estate is involved. For private school owners, that can help make monthly payments more manageable, especially when the project includes a campus purchase, major renovations, or expansion into a larger facility.

Another benefit is the SBA guaranty. For most 7(a) loans, the SBA will guarantee 85% on loans of $150,000 or less and 75% on loans above $150,000. Because that guaranty helps reduce lender risk, qualified private school borrowers may have access to financing options that would be harder to secure through a conventional business loan alone.

There are also some downsides. A big one is the lack of availability for non-profits – a common status for private schools. Another is the size limit – $5 million, which may not be enough for deals involving real estate in high-cost areas. A third is the loan process, which can take longer (45-90 days for standard 7(a) loans, faster for SBA express loans and SBA microloans) and involve more documentation than conventional loans. If any of these are dealbreakers, other loan options may be a better fit.

SBA 7(a) Loans vs. Other Types of Loans for Private Schools

SBA 7(a) Loans vs. Conventional Loans

Both SBA 7(a) loans and conventional business loans may be used to finance private school projects, but they usually serve different borrower profiles.

An SBA 7(a) loan for private schools is designed to help eligible small businesses access funding through approved lenders. The SBA does not lend the money directly. Instead, it provides a guaranty to the lender, which is 85% on loans of $150,000 or less and 75% on loans above $150,000 for most 7(a) loans. That guaranty can make a meaningful difference for qualified school owners who may not receive the same structure through a conventional loan alone.

For private schools, one of the biggest advantages is flexibility. SBA 7(a) funds may be used for eligible real estate, working capital, refinancing business debt, equipment, furniture, fixtures, supplies, and ownership changes. That can be useful when a school project includes more than one need, such as buying an existing private school, upgrading classrooms, investing in technology, and preserving operating cash after closing.

Conventional loans may be a better fit for borrowers with strong financials, a long operating history, substantial collateral, and the ability to qualify without SBA support. They may also be worth considering when the borrower wants to avoid SBA program requirements or needs financing above the standard 7(a) loan maximum of $5 million.

For many private school owners, the decision comes down to the complexity of the project. If the financing need is straightforward and the borrower can qualify easily with a bank, a conventional loan may be competitive. If the project involves a mix of acquisition costs, facility improvements, equipment, and working capital, or if the borrower can’t get acceptable terms from a conventional lender, an SBA 7(a) private school loan may offer a more practical structure.

SBA 7(a) Loans vs. SBA 504 Loans

SBA 7(a) loans and SBA 504 loans are both SBA-backed financing options, but they are not built for the same purpose.

For private schools, the SBA 7(a) program is the more flexible option. It can support eligible uses such as real estate, working capital, equipment, furniture, fixtures, supplies, debt refinancing, and changes of ownership. For private schools, that flexibility can be important when the loan needs to cover both the physical facility and the operating needs tied to growth.

For example, a borrower purchasing a private school may also need funds for classroom improvements, administrative systems, staff transition costs, safety upgrades, supplies, or working capital. A 7(a) loan may allow those needs to be handled through one financing request, depending on eligibility and lender approval.

The SBA 504 loan program is more focused on major fixed assets. It is commonly used for long-term real estate, land, buildings, facility construction, modernization, and certain long-term machinery or equipment. However, 504 loans cannot be used for business acquisition, working capital, or inventory, which can make them less flexible for private school borrowers who need funding beyond the building itself.

There are also structural differences. SBA 504 loans are delivered through Certified Development Companies and are designed for fixed-asset projects. The maximum 504 loan amount is generally $11.25 million, while the standard maximum SBA 7(a) loan amount is $5 million. SBA 504 loans are associated with long-term fixed-rate financing, while 7(a) loans may have fixed or variable rates depending on the lender and loan structure.

For a private school owner, the dividing line is usually the purpose of the funding. If the project is mainly a real estate or fixed-asset purchase and long-term fixed-rate financing is the priority, an SBA 504 loan may be worth reviewing. If the school needs broader financing for acquisition, improvements, equipment, working capital, refinancing, or an ownership transition, the 7(a) program may be the better fit.

Case Study: Private Academy Real Estate Purchase

Nathan owns a for-profit private academy, a K-8 program with 175 enrolled students. The school had outgrown its leased facility, the lease was approaching renewal with a significant rent increase, and the landlord had limited interest in allowing the buildout needed to add science labs and a dedicated arts room.

When a suitable property two miles away came on the market, Nathan saw the chance to move the school into a permanent home that could support the next phase of growth.

The total project cost was $3,450,000:

- Real estate (building and property): $2,800,000

- Renovations (classroom buildout, ADA compliance, HVAC improvements, security systems): $400,000

- Furniture, fixtures, and equipment (desks, lab equipment, technology, playground): $150,000

- Working capital for the transition and move: $100,000

Nathan had $345,000 available for a down payment (10%) and needed financing for the remaining $3,105,000.

He approached three conventional lenders. Two were uncomfortable with the deal due to the construction aspect and a lack of private school loan experience. The third offered to finance the real estate alone but wouldn’t include the renovations, equipment, or working capital. Nathan would have needed separate financing for each, at higher rates and shorter terms.

Through 7aSavvy, Nathan was matched with an SBA 7(a) lender that had experience with education businesses and understood how to evaluate them. The lender was comfortable financing the full project, including the real estate, renovations, equipment, and working capital, in a single loan.

Loan Details:

- Total project cost: $3,450,000

- Down payment: $345,000 (10%)

- Loan amount: $3,105,000

- Interest rate: Prime + 2.25 (9.00% at the time of closing)

- Term: 25 years, fully amortized

- Monthly payment: $26,100

The school was generating annual cash flow of $400,000, giving it a DSCR of 1.28. Growing enrollment, experienced staff, and a clear facilities plan all made the deal a solid fit for the lender. The renovation timeline was structured in phases so the school could continue operating during the transition, with the move completed over summer break.

The loan closed in 75 days. Owning the building eliminated the uncertainty of leasing, and bundling everything into one SBA 7(a) loan saved Nathan from juggling multiple lenders and repayment schedules.

This is an illustrative example based on typical SBA 7(a) loan terms and a realistic private school financing scenario. Actual loan terms, timelines, and outcomes vary based on the borrower, school, and lender.

SBA 7(a) Loan Program History

The SBA 7(a) loan program has long been part of the small business financing landscape in the United States. Its roots go back to the Small Business Act of 1953, which created the U.S. Small Business Administration and established a federal framework for helping small businesses access capital.

The program’s name comes from Section 7(a) of that law. Over the past seven decades it has been the SBA’s primary business loan program, allowing approved lenders to provide financing with the support of an SBA guaranty. By 1954, the agency was already making and guaranteeing loans for small businesses, setting the foundation for the 7(a) program as it is known today.

SBA 7(a) Loan Program Statistics

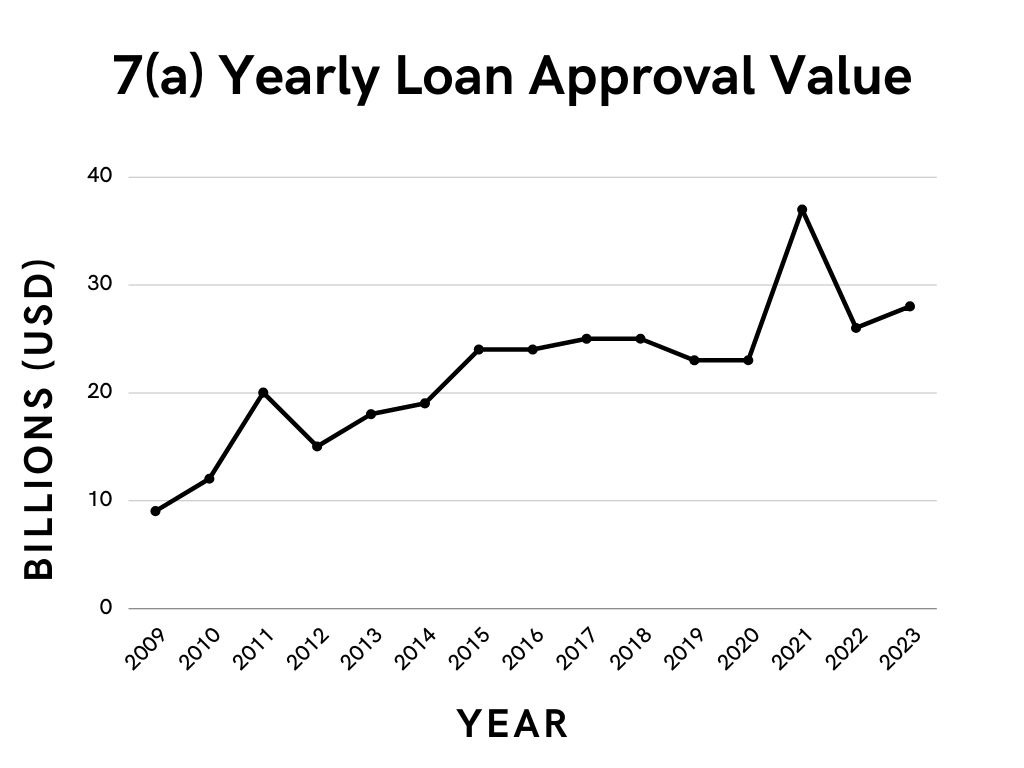

These are the year-by-year* statistics of the SBA 7(a) loan program from Fiscal Year 1992 to today, including the number of 7(a) loans approved and total approval amount.

| Fiscal Year | Loans Approved | Approval Amount |

| 1992 | 23,655 | $5,880,429,292 |

| 1993 | 26,291 | $6,690,995,672 |

| 1994 | 36,049 | $8,142,444,017 |

| 1995 | 55,548 | $8,251,957,812 |

| 1996 | 45,853 | $7,694,062,736 |

| 1997 | 45,288 | $9,461,352,612 |

| 1998 | 42,271 | $9,016,559,155 |

| 1999 | 43,634 | $10,146,109,913 |

| 2000 | 43,748 | $10,523,436,538 |

| 2001 | 42,958 | $9,894,022,393 |

| 2002 | 51,666 | $12,208,026,875 |

| 2003 | 67,306 | $11,268,200,031 |

| 2004 | 81,133 | $13,571,560,391 |

| 2005 | 95,900 | $15,223,525,886 |

| 2006 | 97,291 | $14,525,100,339 |

| 2007 | 99,606 | $14,292,141,213 |

| 2008 | 69,437 | $12,671,235,790 |

| 2009 | 41,288 | $9,191,044,339 |

| 2010 | 47,000 | $12,406,048,700 |

| 2011 | 53,710 | $19,640,298,400 |

| 2012 | 44,376 | $15,153,504,000 |

| 2013 | 46,395 | $17,865,672,500 |

| 2014 | 52,044 | $19,190,547,800 |

| 2015 | 63,461 | $23,583,863,400 |

| 2016 | 64,074 | $24,128,426,343 |

| 2017 | 62,430 | $25,447,458,500 |

| 2018 | 60,354 | $25,372,539,100 |

| 2019 | 51,907 | $23,175,811,000 |

| 2020 | 42,298 | $22,549,825,700 |

| 2021 | 51,856 | $36,536,756,800 |

| 2022 | 47,678 | $25,693,805,700 |

| 2023 | 57,362 | $27,515,666,000 |

| 2024 | 70,242 | $31,124,036,200 |

| 2025 | 78,078 | $37,287,816,200 |

Source: SBA, 7(a) & 504 FOIA

*U.S. Federal Government fiscal years

SBA 7(a) Loans On the Rise

The SBA 7(a) loan program has seen outstanding recent growth, with the annual total value of approved loans tripling in the last 15 years. Not bad for a program that’s been around since 1953!