Fiscal Year 2025

764

Loans Approved

$2.0B

Total Value

Running or acquiring a hotel takes more than vision. It takes capital that fits the realities of hospitality, from property costs and upgrades to working capital for day-to-day operations. That is where an SBA 7(a) hotel loan can make sense.

The SBA 7(a) program is the U.S. Small Business Administration’s primary loan program for small businesses. These loans are issued by approved lenders, not directly by the SBA, but the SBA provides a guaranty that helps reduce lender risk. For most 7(a) loans, that guaranty is up to 85% on loans of $150,000 or less and up to 75% on loans above $150,000. That added protection can make lenders more willing to finance qualified hotel borrowers that may not fit the box for a conventional commercial loan.

For hotel owners, flexibility is one of the biggest advantages of the program. SBA states that 7(a) funds can be used for acquiring, refinancing, or improving real estate and buildings, as well as working capital, refinancing current business debt, equipment, furniture, fixtures, and supplies, and even changes of ownership. In practical terms, that means an SBA 7(a) hotel loan may help finance a hotel purchase, property improvements, FF&E updates, or operational needs tied to opening, stabilizing, or expanding the business.

Why Hotel Owners Look at SBA 7(a) Financing

Hotel financing is rarely simple. Lenders often have to consider property performance, borrower experience, brand standards, seasonal revenue swings, renovation plans, and whether the business will be owner-operated or investor-led. A standard bank loan may work for some deals, but an SBA 7(a) hotel loan can be attractive when the project needs more flexible underwriting and a repayment structure built for small business ownership.

Because the program can support both real estate-related uses and operating needs, it is often considered by borrowers who want one financing solution that covers more than just the purchase price. Depending on the deal, that can include acquisition costs, soft costs, upgrades, furniture, working capital, or a partner buyout. The SBA explicitly lists multiple-purpose loans among permitted 7(a) uses.

Uses of SBA 7(a) Loans for Hotels

An SBA 7(a) hotel loan may be used for situations like:

Hotel Acquisition

Buying an existing hotel is one of the most common reasons borrowers explore the program. This can include independent properties, limited-service hotels, boutique assets, and franchised hotels, depending on eligibility and lender appetite.

Renovations and Property Improvements

Hotels often need capital for room refreshes, lobby renovations, exterior updates, operational improvements, or compliance-related property work. The SBA allows 7(a) proceeds to be used for improving real estate and buildings.

Furniture, Fixtures, and Equipment

Hospitality properties routinely require spending on beds, case goods, laundry equipment, kitchen items, security systems, technology upgrades, and other operating assets. The SBA includes the purchase of machinery and equipment plus furniture, fixtures, and supplies among eligible uses.

Working Capital

Seasonality, payroll, inventory, marketing, and ramp-up periods can all create pressure on cash flow. The SBA states that 7(a) loans for hotels can be used for both short- and long-term working capital.

Debt Refinance

Some hotel owners use the program to refinance business debt into a structure that better fits the property’s cash flow. The SBA lists refinancing current business debt as an eligible use of proceeds.

Change of Ownership

If the transaction involves buying out a partner, purchasing a hotel business from an existing owner, or facilitating a full or partial transition, the SBA also permits 7(a) financing for changes of ownership.

SBA 7(a) Loans for Hotels Terms and Eligibility

How Much Can You Borrow?

The standard maximum loan amount under the SBA 7(a) program is $5 million. That does not mean every hotel project will qualify for that amount, but it gives small hospitality businesses meaningful room to finance acquisitions, improvements, refinancing, or a combination of uses.

Repayment Terms and Prepayment Rules

Repayment terms under the 7(a) program vary based on how the proceeds are used. For loans involving real estate, the SBA allows terms of up to 25 years, which can help reduce monthly debt service compared with shorter-term structures.

Borrowers should also understand the prepayment rule. The SBA states that for hotel 7(a) loans with a maturity of 15 years or longer, a prepayment penalty applies only if the borrower voluntarily prepays 25% or more of the outstanding balance during the first three years after first disbursement. The penalty is 5% in year one, 3% in year two, and 1% in year three.

That is especially relevant for hotel borrowers thinking ahead to refinancing after stabilization or selling the property within a few years.

Eligibility and Qualifications

The 7(a) program is designed for small businesses that meet SBA rules. The SBA says eligible businesses generally must:

- be an operating business

- operate for profit

- be located in the United States

- meet SBA size standards

- show a need for the requested credit

- demonstrate that the loan proceeds will be used for a sound business purpose

The lender also looks at creditworthiness and repayment ability.

For hotels, the underwriting conversation usually goes beyond basic eligibility. Lenders may also focus on occupancy trends, ADR and RevPAR performance, property condition, management experience, franchise status, renovation scope, and whether the project’s projected cash flow supports the debt.

Important note:

Meeting these basic requirements does not guarantee approval. Final SBA 7(a) hotel loan eligibility also depends on factors such as the type of business, use of proceeds, credit profile, repayment ability, and overall lender underwriting criteria.

SBA 7(a) Loans for Hotels: Pros and Cons

An SBA 7(a) hotel loan can offer more than funding. It can provide a financing structure that better fits how hospitality businesses actually operate. SBA allows 7(a) funds to be used for hotel acquisition, property improvements, equipment, working capital, debt refinance, and ownership changes, giving borrowers more flexibility than many narrower loan products.

The program may also offer longer repayment terms, including up to 25 years for real estate, which can improve monthly payment affordability. And because the SBA guarantees a large share of the loan for the lender, qualified borrowers may find it easier to access financing than they would through a conventional loan alone. SBA guarantees up to 85% on loans of $150,000 or less and up to 75% on loans above $150,000.

For hotel borrowers who want help finding the right lender, 7aSavvy is a lender-matching platform for SBA 7(a) loans and its process is free for borrowers, which can make the search more efficient from the start.

The downsides are that the program has a loan cap, may come with higher rates than the best conventional loan options, and typically involves a more detailed approval process. Even so, for many small hotel projects, SBA 7(a) hotel financing remains appealing because it balances versatility, accessibility, and long-term affordability.

SBA 7(a) Loans vs. Other Types of Loans for Hotels

SBA 7(a) Loans vs. Conventional Loans

Both SBA 7(a) loans and conventional business loans can be used to finance hotel projects, but they are built for different kinds of borrowers and different lending situations.

The SBA 7(a) program is designed to help small businesses access capital through approved lenders, with the SBA guaranteeing up to 85% of loans of $150,000 or less and up to 75% of loans above $150,000 for most 7(a) loans. That guaranty can make the program more accessible for qualified borrowers who may not receive the same terms through a conventional loan alone. SBA also requires 7(a) applicants to show they are not able to obtain the desired credit on reasonable terms from non-government sources, which underscores that the program is meant to fill gaps in the conventional market.

Conventional loans, by contrast, may work best for borrowers with stronger balance sheets, strong operating history, and the ability to qualify without SBA support. They may also be attractive when a borrower does not want SBA program rules or when the financing need exceeds the 7(a) program’s $5 million cap.

For many hotel borrowers, the decision comes down to attainability and structure. If the project is unlikely to get conventional financing at a reasonable interest rate, or needs a repayment term of up to 25 years for real-estate-backed financing, the SBA 7(a) route may be the better match. If the borrower can qualify comfortably through a conventional lender and does not need the SBA framework, conventional financing may be worth comparing alongside it.

Since the 7aSavvy platform focuses on SBA 7(a) lender matching, it can be useful for borrowers who want to explore whether an SBA-backed structure makes more sense than going straight to the conventional market.

SBA 7(a) Loans vs. SBA 504 Loans

Although both are SBA-backed programs, SBA 7(a) loans and SBA 504 loans serve different purposes, and that distinction matters for hotel borrowers.

The 7(a) program is the more flexible of the two. SBA 7(a) funds may be used for real estate, working capital, debt refinance, equipment, furniture, fixtures, supplies, ownership changes, and multiple-purpose loans. That makes it a strong option when a hotel transaction includes a mix of needs, such as buying the property, refreshing rooms, covering soft costs, and maintaining operating liquidity after closing.

The 504 loan program is narrower – long-term, fixed-rate financing for major fixed assets that promote business growth and job creation. The SBA also states that 504 loans can be used for assets such as existing buildings or land, new facilities, long-term machinery and equipment, and modernization of existing facilities, but cannot be used for working capital or inventory.

That difference is especially important in hospitality. A hotel acquisition often includes not just the real estate, but also liquidity needs around staffing, marketing, reserves, operating ramp-up, and other expenses. If the financing package needs to cover those broader business purposes, 7(a) is often the more practical structure because the SBA explicitly allows working capital and multiple-purpose uses under that program.

There are also structural differences. SBA 504 financing is delivered through Certified Development Companies (CDCs), and the program is built specifically for fixed-asset projects. 504 loans are available at values up to $11.25 million, while the maximum standard 7(a) loan amount is $5 million. SBA also describes 504 loans as partly fixed rate, while 7(a) interest rates may be fixed or variable depending on the loan.

For hotel borrowers, that usually leads to a simple dividing line. If the financing need is centered on a major fixed-asset project and long-term fixed-rate financing is the priority, a 504 loan may deserve a close look. If the hotel deal needs broader flexibility, mixed uses of proceeds, or a single loan that can address both property and business needs, the 7(a) program is often the better fit.

Because that choice is not always obvious at the start, many borrowers prefer to begin with lender guidance. 7aSavvy is a lender-matching platform for SBA 7(a) borrowers, which can be useful when the goal is to understand whether a hotel project fits better in the 7(a) lane before pursuing a lender directly.

Case Study: Independent Hotel Acquisition

Marcus had spent 12 years managing hotels for a hospitality group, working his way from the front desk all the way to general manager. When a 45-room independent hotel came up for sale, Marcus saw the opportunity to step into ownership.

The property was well-located in a coastal vacation destination, but aging. Occupancy was still solid at 72% with an ADR of $125, driven by the location and repeat guests, but the rooms hadn’t been updated in over a decade. Marcus planned to keep the property running during a phased renovation, refreshing 10-15 rooms at a time while maintaining revenue from the rest of the hotel.

The total project cost was $3,600,000:

- Hotel purchase price (real estate, business, and existing FF&E): $3,200,000

- Room renovations and FF&E updates: $300,000

- Working capital for the transition and ramp-up period: $100,000

Marcus had $360,000 available for a down payment (10%) and needed financing for the remaining $3,240,000.

He approached two conventional lenders. The responses were discouraging. Hotels are classified as special-purpose properties, a factor that makes many conventional lenders cautious. Both banks required 25-30% down, which would have meant $900,000 to $1,080,000. One was also uncomfortable with the seasonal revenue pattern typical of a coastal market and declined outright.

Through 7aSavvy, Marcus was matched with an SBA 7(a) lender that had funded hotel acquisitions before and understood the dynamics of seasonal hospitality properties. The lender was comfortable with the occupancy trends, the phased renovation plan, and Marcus’s management track record in the industry.

Loan Details:

- Total project cost: $3,600,000

- Down payment: $360,000 (10%)

- Loan amount: $3,240,000

- Interest rate: Prime + 1.75 (8.50% at the time of closing)

- Term: 25 years, fully amortized

- Monthly payment: $26,089

The hotel was generating annual cash flow of $420,000, giving it a DSCR of 1.34. The solid financials, Marcus’s track record in the industry, and the renovation plan all contributed to the loan being approved.

The loan closed in 81 days. By combining the acquisition, renovations, and working capital into a single SBA 7(a) loan, Marcus avoided the hassle and cost of piecing together separate financing for each component. The 10% down payment preserved enough of his capital to cover operating costs during the ownership transition, including staffing changes and vendor renegotiations.

This is an example based on typical SBA 7(a) loan terms and a realistic hotel acquisition scenario. Actual loan terms, timelines, and outcomes vary based on the borrower, property, and lender.

SBA 7(a) Loan Program History

The SBA 7(a) loan program traces back to the Small Business Act of 1953, the law that created the U.S. Small Business Administration and established the framework for federal support of small business lending. The program takes its name from Section 7(a) of that law and grew into the SBA’s primary loan program over time. SBA’s own history notes that by 1954 the agency was already making and guaranteeing loans for small businesses, laying the groundwork for what would become one of the country’s best-known small business financing programs. Today, 7(a) remains the SBA’s flagship lending program, built to help small businesses access capital through private lenders with the support of an SBA guaranty.

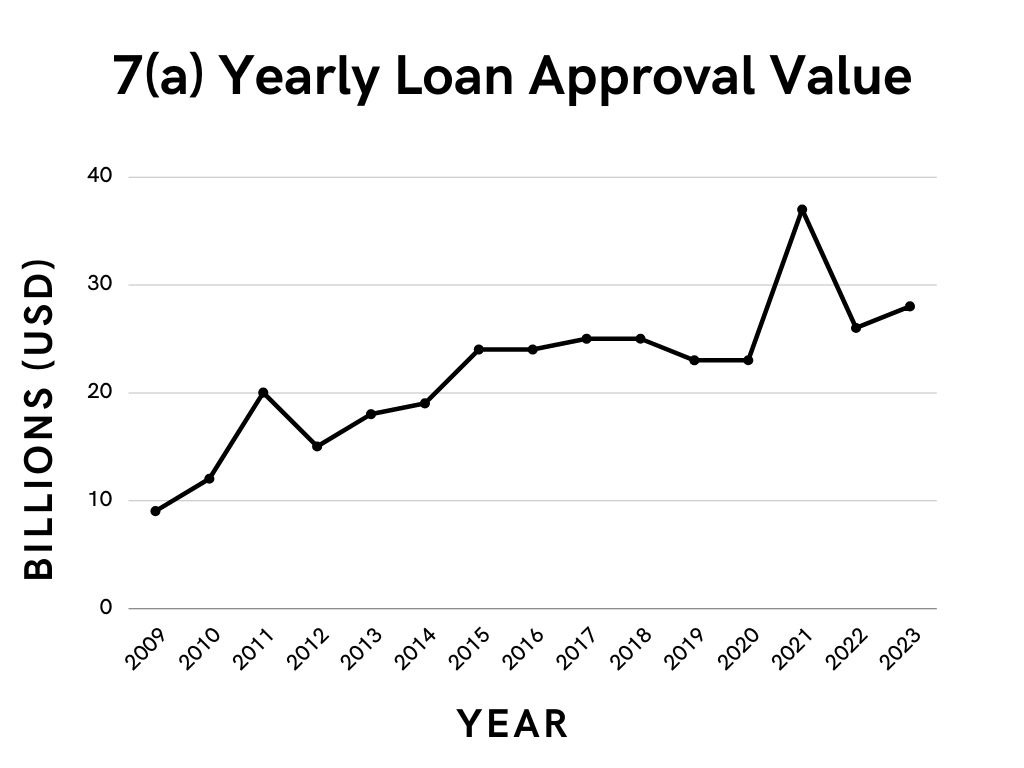

SBA 7(a) Loan Program Statistics

These are the year-by-year* statistics of the SBA 7(a) loan program from Fiscal Year 1992 to today, including the number of 7(a) loans approved and total approval amount.

| Fiscal Year | Loans Approved | Approval Amount |

| 1992 | 23,655 | $5,880,429,292 |

| 1993 | 26,291 | $6,690,995,672 |

| 1994 | 36,049 | $8,142,444,017 |

| 1995 | 55,548 | $8,251,957,812 |

| 1996 | 45,853 | $7,694,062,736 |

| 1997 | 45,288 | $9,461,352,612 |

| 1998 | 42,271 | $9,016,559,155 |

| 1999 | 43,634 | $10,146,109,913 |

| 2000 | 43,748 | $10,523,436,538 |

| 2001 | 42,958 | $9,894,022,393 |

| 2002 | 51,666 | $12,208,026,875 |

| 2003 | 67,306 | $11,268,200,031 |

| 2004 | 81,133 | $13,571,560,391 |

| 2005 | 95,900 | $15,223,525,886 |

| 2006 | 97,291 | $14,525,100,339 |

| 2007 | 99,606 | $14,292,141,213 |

| 2008 | 69,437 | $12,671,235,790 |

| 2009 | 41,288 | $9,191,044,339 |

| 2010 | 47,000 | $12,406,048,700 |

| 2011 | 53,710 | $19,640,298,400 |

| 2012 | 44,376 | $15,153,504,000 |

| 2013 | 46,395 | $17,865,672,500 |

| 2014 | 52,044 | $19,190,547,800 |

| 2015 | 63,461 | $23,583,863,400 |

| 2016 | 64,074 | $24,128,426,343 |

| 2017 | 62,430 | $25,447,458,500 |

| 2018 | 60,354 | $25,372,539,100 |

| 2019 | 51,907 | $23,175,811,000 |

| 2020 | 42,298 | $22,549,825,700 |

| 2021 | 51,856 | $36,536,756,800 |

| 2022 | 47,678 | $25,693,805,700 |

| 2023 | 57,362 | $27,515,666,000 |

| 2024 | 70,242 | $31,124,036,200 |

| 2025 | 78,078 | $37,287,816,200 |

Source: SBA, 7(a) & 504 FOIA

*U.S. Federal Government fiscal years

SBA 7(a) Loans On the Rise

The SBA 7(a) loan program has seen outstanding recent growth, with the annual total value of approved loans tripling in the last 15 years. Not bad for a program that’s been around since 1953!